Most Employees Leave Thousands in Free 401(k) Match on the Table Every Year

The average employer match is worth $1,336 per year — yet 1 in 4 employees contributes too little to capture it fully. This guide explains how the 401(k) system actually works, what the 2025 limits mean for your paycheck, and how to use our free calculator to find exactly how much free money you're leaving unclaimed.

What Is a 401(k) Plan and Why It Matters for Retirement

A 401(k) is an employer-sponsored retirement savings plan named after the section of the U.S. tax code that created it. Importantly, it's one of the most powerful retirement planning tools available to American workers. Furthermore, understanding how it works is essential for building long-term financial security. Moreover, the tax advantages make 401(k) plans dramatically superior to regular savings accounts for retirement funding.

The fundamental concept is straightforward: you contribute money from your paycheck before taxes are calculated, reducing your current taxable income. Consequently, you save on income taxes while simultaneously building retirement savings. Additionally, many employers match a percentage of your contributions, effectively providing free money for retirement. Therefore, not maximizing a 401(k) match represents lost opportunity worth thousands of dollars annually.

💡 How 401(k) Plans Work: The Complete Mechanics

When you enroll in a 401(k), you specify how much to contribute from each paycheck, up to annual limits. Notably, these contributions are deducted before income taxes are calculated, lowering your taxable income. Additionally, your employer may contribute a matching amount based on your contribution level—typically 50-100% of your contributions up to 3-6% of salary. Consequently, this employer match is immediate returns on your money.

Your contributions and employer match grow in the investment accounts you select within the plan. Furthermore, all growth is tax-deferred, meaning you pay no taxes on investment gains until you withdraw in retirement. Specifically, when you withdraw after age 59½, withdrawals are taxed as ordinary income. Additionally, withdrawals before 59½ typically incur a 10% early withdrawal penalty plus income taxes, with limited exceptions for hardship. Therefore, 401(k)s are designed as long-term retirement vehicles, not emergency funds.

🎯 Tax Advantages of 401(k) Plans

The tax benefits of 401(k) plans are substantial. First, pre-tax contributions reduce your current taxable income dollar-for-dollar. For example, a $10,000 contribution reduces taxable income by $10,000. Furthermore, if you're in the 24% tax bracket, this saves $2,400 in immediate taxes. Additionally, this tax savings can be reinvested or used for other purposes. Moreover, this tax advantage represents perhaps the biggest advantage of 401(k) plans versus regular savings accounts.

Second, investment growth within the 401(k) is tax-deferred. Specifically, if an investment grows from $10,000 to $15,000, you owe no taxes on the $5,000 gain until you withdraw in retirement. Consequently, compound growth accelerates because you're earning returns on your full account balance, not just the after-tax portion. Additionally, over decades, tax deferral can result in significantly larger retirement nest eggs. Therefore, the long-term benefits are enormous for disciplined savers.

Historical Evolution: From Pensions to 401(k) Plans

Before the 401(k) era, most American workers relied on pension plans provided by employers. In fact, pensions were the primary retirement vehicle from the 1940s through the 1970s. Furthermore, these defined-benefit pensions guaranteed specific monthly retirement income based on salary and years of service. Notably, employers bore all investment risk and responsibility for paying promised benefits.

The dramatic shift occurred in 1978 when Congress created the 401(k) option as a supplemental retirement savings vehicle. Subsequently, what was intended as a supplement to pensions became the dominant retirement plan structure. Moreover, employers quickly recognized that 401(k) plans shifted investment risk and burden from the company to employees. Consequently, companies enthusiastically replaced pension plans with 401(k) plans, creating a fundamental transformation in American retirement security.

Today, 401(k) plans dominate American retirement planning. Specifically, over $7 trillion is held in 401(k) accounts, making them the second-largest retirement savings vehicle after IRAs. Furthermore, this represents a complete reversal from the pension-dominated system of previous decades. Notably, workers today bear all investment risk—they must select investments and manage their portfolios, unlike pension recipients who received guaranteed income. Consequently, financial literacy is more important than ever for retirement success.

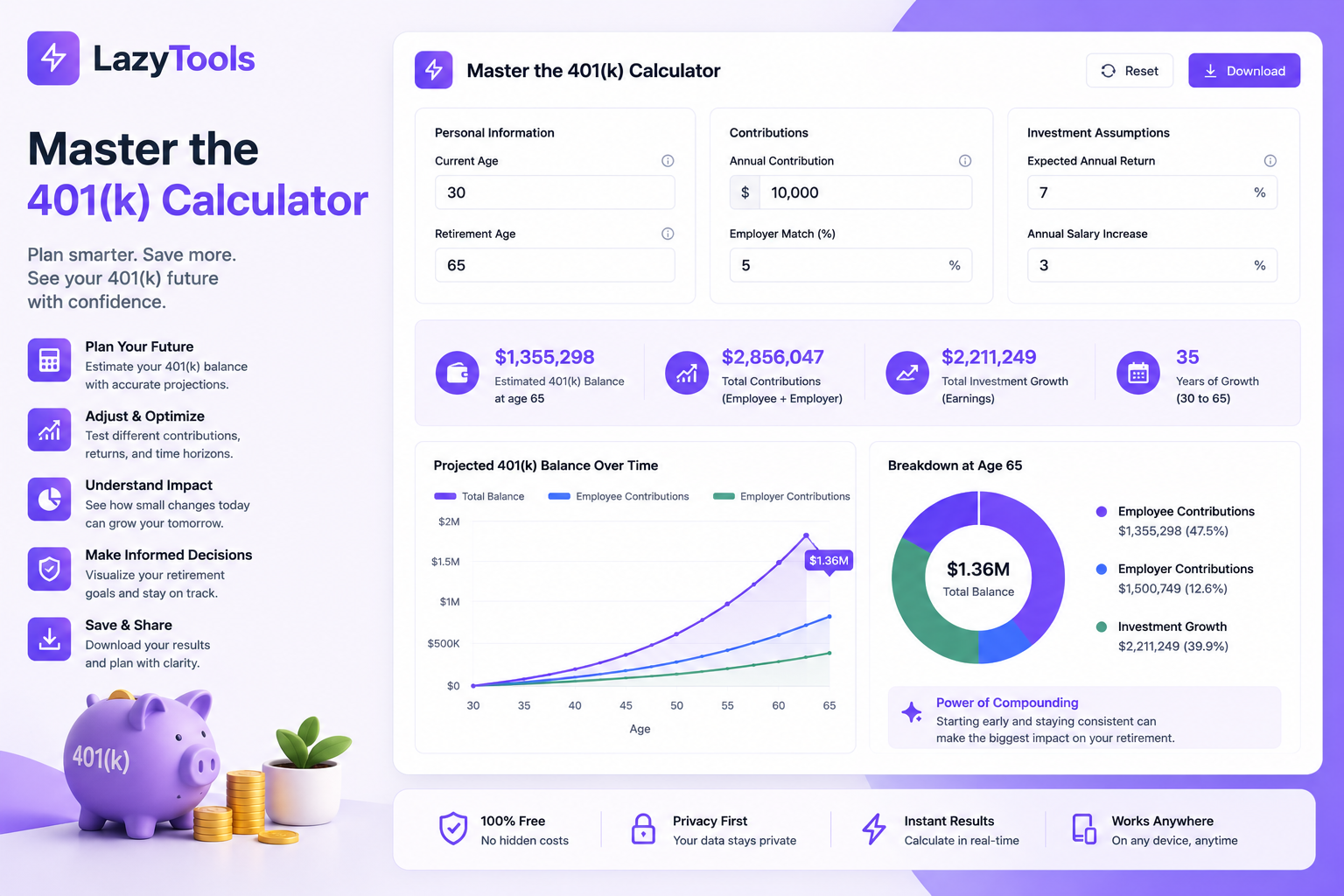

How to Use Our 401(k) Calculator: Step-by-Step Guide

Our free 401(k) calculator simplifies retirement planning into an intuitive four-step process. Importantly, it accounts for employer matching, contribution limits, and various tax scenarios. Furthermore, it projects how your contributions will grow over decades. Additionally, you can experiment with different contribution levels to see the financial impact.

💼 Real-World Example: The Power of Employer Match

Consider Sarah earning $60,000 annually. Specifically, her employer offers a 100% match on contributions up to 3% of salary. If Sarah contributes 3% ($1,800/year), her employer contributes another $1,800—instant 100% return. Furthermore, if Sarah contributes only 1%, she only receives $600 employer match, leaving $1,200 in free money on the table. Therefore, understanding and maximizing employer match is critical.

🎯 Plan Your Retirement Today

Calculate contributions, maximize employer match, plan for retirement. Completely free, no signup required.

Essential 401(k) Calculator Features for Smart Retirement Planning

2024-2025 401(k) Contribution Limits and Key Regulatory Information

Understanding current contribution limits is essential for effective 401(k) planning. Additionally, limits change annually and vary based on age. Specifically, here are the 2024-2025 limits:

| Category | 2024 Limit | 2025 Limit | Key Details |

|---|---|---|---|

| Employee Contribution | $23,500 | $24,000 | Annual limit per employee |

| Catch-Up (Age 50+) | $7,500 | $8,000 | Additional amount for older workers |

| Combined Employee+Employer | $69,000 | $71,000 | Total limit including match |

| Highly Compensated Employee | $150,000 | $155,000 | Income threshold for special rules |

| Early Withdrawal Penalty | 10% | 10% | Plus income taxes on amount withdrawn |

| Required Minimum Distribution | Age 73 | Age 73 | Starting age for mandatory withdrawals |

Pro Insight: Importantly, if your employer offers a match, prioritize contributing enough to capture the full match first. Furthermore, any additional contributions should maximize the full $24,000 limit if financially possible. Additionally, those age 50+ should consider maxing out catch-up contributions for accelerated retirement savings.

What People Search For: 401(k) Questions Answered

Based on common search queries, here are the questions people ask most frequently about 401(k) plans. Moreover, these questions reveal critical retirement planning concerns:

❓ "How much should I contribute to my 401(k)?"

Financial advisors typically recommend contributing 10-15% of gross salary for retirement security. Importantly, if your employer offers a match, prioritize capturing the full match first—this is immediate free money. Furthermore, a common baseline is contributing 3-6% (just enough for the match), then increasing contributions 1% annually until you reach 10-15% or hit the $24,000 limit. Specifically, this balanced approach optimizes employer match while building adequate retirement savings.

❓ "What is an employer 401(k) match and why does it matter?"

An employer match is free money your employer contributes to your 401(k) based on your contributions. Notably, common match formulas include 50% match up to 3% of salary or 100% match up to 6% of salary. Therefore, if your employer offers a 100% match up to 6%, not contributing 6% means leaving 6% of your salary on the table. Furthermore, this represents thousands of dollars in lost free money over your career. Consequently, maximizing employer match should be a top financial priority.

❓ "Can I withdraw from my 401(k) before retirement?"

Early withdrawals before age 59½ typically incur a 10% penalty plus income taxes on the withdrawn amount. Specifically, if you withdraw $10,000 at age 45 in the 24% tax bracket, you owe $2,400 in taxes plus $1,000 penalty ($11,000 total cost). Additionally, some plans allow loans against your 401(k) balance with better terms than early withdrawals. Importantly, 401(k)s should be treated as long-term retirement vehicles, not emergency funds—use emergency savings instead.

❓ "What's the difference between traditional and Roth 401(k)?"

Traditional 401(k)s use pre-tax contributions (reducing current taxes) with taxes owed in retirement. Conversely, Roth 401(k)s use after-tax contributions (no current tax reduction) with tax-free growth and withdrawals. Specifically, traditional plans help workers who expect lower tax brackets in retirement, while Roth plans benefit those expecting higher brackets. Furthermore, choosing between them depends on current income, retirement timeline, and tax predictions. Most importantly, contributing to either is far better than not contributing at all.

❓ "How much will my 401(k) grow if I start now?"

Growth depends on contributions, employer match, investment returns, and time horizon. Specifically, someone contributing $10,000 annually with 3% employer match and 7% annual returns would accumulate approximately $200,000 over 10 years, $550,000 over 20 years, and $1.3 million over 30 years. Furthermore, these projections demonstrate the power of compound growth. Importantly, starting early dramatically increases final retirement nest egg. Consequently, even modest contributions started young can grow into substantial retirement savings.

How AI and Machine Learning Optimize Retirement Planning

Modern retirement planning increasingly incorporates artificial intelligence and machine learning. Furthermore, these technologies are revolutionizing how people make investment and savings decisions. Notably, AI-powered retirement systems provide personalized guidance that was previously available only to wealthy individuals hiring personal advisors.

🧠 Intelligent Contribution Recommendations

Traditional advice is generic: "Contribute 10-15% of salary." By contrast, AI algorithms analyze your specific situation—current age, salary trajectory, family circumstances, other assets, and retirement goals. Specifically, they calculate the exact contribution percentage needed to reach your retirement target. Furthermore, they adjust recommendations as circumstances change. Consequently, AI-driven recommendations are far more personalized than generic rules of thumb. Moreover, studies show that personalized recommendations increase retirement savings by 20-30% versus generic advice.

📊 Dynamic Investment Allocation Intelligence

AI systems now automatically optimize investment allocation within 401(k)s based on your age, risk tolerance, and time horizon. Importantly, they rebalance automatically without human intervention. Furthermore, they adjust allocation as you approach retirement—automatically reducing risk through target-date fund logic. Additionally, some advanced systems use machine learning to identify optimal fund selections from dozens of available choices. Consequently, workers benefit from professional-grade portfolio management at no additional cost beyond their 401(k) plan fees.

💡 Scenario Planning and What-If Analysis

AI-powered calculators instantly model thousands of scenarios: different contribution levels, market conditions, retirement dates, and spending patterns. Specifically, you can ask "What if I contribute 15% instead of 10%?" or "What if markets return 4% instead of 7%?" and see instant results. Furthermore, this exploration helps you understand cause-and-effect relationships. Additionally, people armed with this knowledge make better financial decisions. Therefore, AI transforms abstract concepts into tangible, understandable projections.

🎯 Behavioral Economics Insights

Advanced systems use behavioral economics research to automatically increase contributions over time. Specifically, many use "auto-escalation"—automatically increasing your contribution percentage 1% per year until reaching a target. Furthermore, this leverages behavioral economics findings that people prefer automatic changes over making decisions themselves. Consequently, contribution rates increase from average 3-4% to optimal 10-15% without requiring annual decision-making. Moreover, studies show auto-escalation increases final retirement savings by 25-50%.

Advanced 401(k) Strategies for Maximum Retirement Savings

Beyond basic contributions, sophisticated strategies can significantly accelerate retirement savings. Furthermore, these approaches are accessible to most workers. Notably, combining multiple strategies creates powerful compounding effects:

🎯 Strategy 1: Maximize the Match First

Prioritize contributing enough to capture 100% of your employer's match. Specifically, this is the highest "guaranteed return" available. For example, a 100% match up to 6% returns 100% on your money—impossible to beat in markets. Furthermore, this should be the first funding priority before investing elsewhere. Additionally, failure to capture full match represents literally leaving money on the table.

📈 Strategy 2: Annual Increase of 1% per Year

After capturing the match, increase your contribution 1% per year. Specifically, if you start at 3%, increase to 4% next year, then 5%, until reaching 10-15%. Moreover, this approach is painless because salary increases typically exceed 1%, making increases imperceptible. Furthermore, this automatic escalation produces substantial savings without lifestyle reduction. Consequently, many people reach 15% contributions over 10-12 years through this method.

💰 Strategy 3: Direct Windfalls to 401(k)

When you receive bonuses, raises, or tax refunds, redirect a portion to 401(k) contributions. Specifically, if you receive a $3,000 raise, increase 401(k) contributions rather than spending the raise. Furthermore, this allows maximum contributions without reducing take-home pay. Additionally, this strategy dramatically accelerates retirement savings without feeling like sacrifice. Importantly, it combines behavioral economics (using "found money") with powerful savings acceleration.

🔄 Strategy 4: Job-Change Rollovers

When changing jobs, roll your 401(k) to an IRA or new employer's 401(k) rather than cashing out. Specifically, cashing out triggers income taxes and 10% penalties if you're under 59½. Consequently, a $100,000 balance could become only $76,000 after taxes and penalties. Furthermore, rollovers preserve the full amount and maintain tax-deferred growth. Additionally, rollovers provide more investment control in IRAs. Therefore, always roll over when changing employers.

🎯 Strategy 5: Roth Conversion (for Higher Earners)

Higher-income workers may benefit from Roth conversions—converting traditional 401(k) balances to Roth IRAs. Specifically, this creates tax diversification and enables tax-free growth on converted amounts. Furthermore, conversions pay taxes in the conversion year but provide tax-free withdrawals in retirement. Additionally, this strategy works best in low-income years (between jobs, sabbaticals, or early retirement). Importantly, consult a tax professional before attempting conversions due to complex rules.

🧓 Strategy 6: Max Out Catch-Up Contributions at 50

Starting at age 50, you can contribute an additional $8,000 annually as catch-up contributions. Specifically, this brings your total from $24,000 to $32,000—a 33% increase. Furthermore, for those behind on retirement savings, catch-up contributions provide acceleration opportunity. Additionally, catch-up years (ages 50-67) represent your final opportunity for high contributions before required distributions begin. Importantly, workers age 50+ should seriously consider maxing out catch-up if financially possible.

Authoritative 401(k) and Retirement Planning Resources

To deepen your knowledge of 401(k) planning and retirement strategies, explore these authoritative sources. Furthermore, these organizations provide reliable information and industry standards:

🏛️ Government Resources

- IRS 401(k) Information — Official contribution limits and rules

- Department of Labor EBSA — Employee Benefits Security Administration guidance

- SEC Investor.gov — Investment education and protections

💼 Professional Organizations

- CFP Board — Certified Financial Planner certifications and education

- NAPFA — Fee-only financial advisor association

- AARP Retirement Planning — Retirement resources for older workers

📚 Educational Resources

- Investopedia — 401(k) education and financial literacy

- Khan Academy Finance — Free retirement planning courses

- Bogleheads Forum — Community for long-term investors